Snapchat is working on a new 'Snapchat+' subscription service, providing exclusive access to upcoming features.

Similar to Twitter Blue, but with potentially more appealing features for Snapchat users.

It's against this background that this application is looking for a new revenue generation source, one that takes form through a subscription service called 'Snapchat+', which users will have access to a whole new level of exclusive and experimental app features and tools, at a time when rising pressure on revenue recently led the app to issue a profit warning last month.

Variable pricing tiers, though, there's also a free, one-week trial option available to let you take the service out for a spin and see what's on offer.

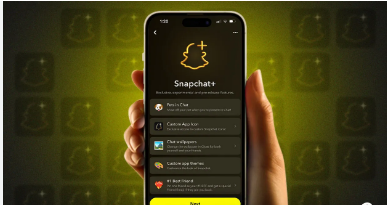

For now, in this early iteration, that offering includes:

Exclusive access to Snapchat icons

A new profile badge that lets others know you're a Snapchat+ user

New data insights, for example, the ability to see who has been at a friend's location (over the past 24 hours), and details about who has rewatched your Story

Ability to pin a user in the app as 'your #1 best friend'

Those aren't exactly earth-shattering additions – but again, this is early days, and it could change a lot between now and an official release, if it actually gets to that stage.

We asked Snapchat about Snapchat + and it provided the following statement:

"We're doing early internal testing of Snapchat+, a new subscription service for Snapchatters. We're excited about the potential to share exclusive, experimental, and pre-release features with our subscribers, and learn more about how we can best serve our community."

Effectively, it's Twitter Blue, but with Snapchat - at least if current Twitter Blue take-up is anything to go by, it won't be a tremendous hit, at least in most users' eyes.

In its latest quarter performance update, the company reported that revenue from subscription and other non-advertising sources stood at $94 million in Q4 21, which actually reflects a 31% year-over-year decrease. This would mean that in all probability, Twitter Blue is yet to gain any traction while Twitter CEO Parag Agrawal has also stated that Twitter has not even hit "intermediate milestones that enable confidence" with its new revenue and growth projects.

Perhaps, part of the reason Snap might feel a little more confident is that Snapchat is that kind of an app that the user finds personally aligned with their requirements-the user ends up having a pretty strong affiliation with the platform for private messaging and interaction purposes. For example, in the case of Snap streaks, users try to keep their daily interactions alive and sometimes at all costs. That shows that users appear to have a more effective relationship with Snapchat than with any other apps.

Perhaps that might make more people accept the registration, and the additional information would also be something of a magnet for users interested in keeping track of their links better.

That could actually be a pretty strong selling point, more so than what Twitter Blue has in the hopper – though again, it's early days, probably too early to say exactly what the actual offering will be in the end.

But Snap has to try new things.

As noted, last month, Snapchat issued a guidance note to the SEC which advised that its overall revenue would miss the targets that it communicated in its Q1 earnings update, which it reported just a month earlier.

As Snap said,

Since we issued guidance on April 21, 2022, the macroeconomic environment deteriorated much faster than we could have anticipated. Accordingly, we believe it is likely that we will report revenue and adjusted EBITDA below the low end of our Q2 2022 guidance range.

Is subscription a possibility to prop up the revenue of Snap and keep it in step with others - like AR Spectacles?

This seems to bring a bit of value for the users to Snap, maybe even more than what Twitter has seen. We'll keep you updated on any progress.